Dubai: Do you have a business in the UAE that’s heading into a merger or acquisition deal? Or about to go in for a corporate restructuring?

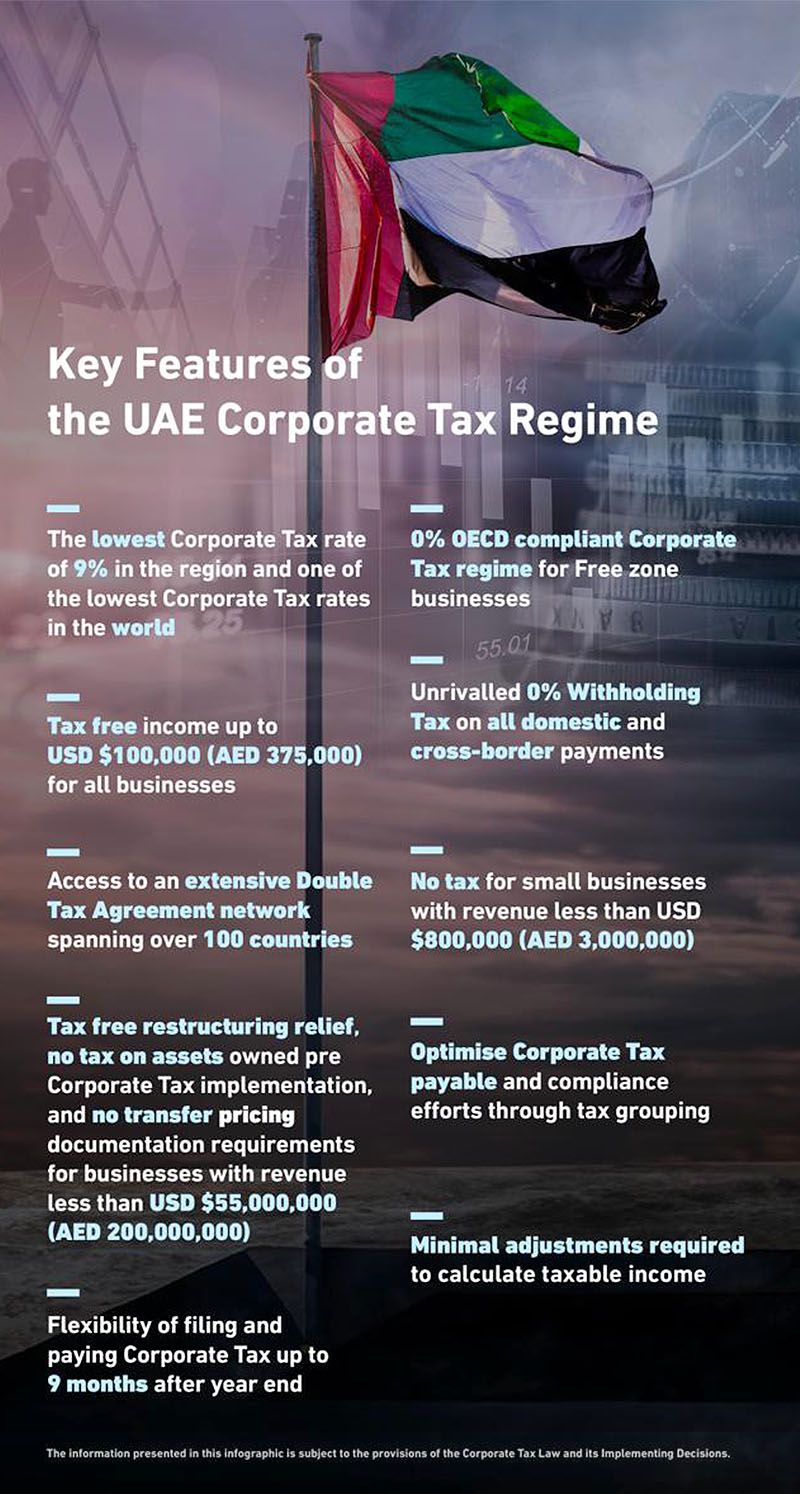

Then, the business becomes eligible for corporate tax relief, among some of the benefits that the Ministry of Finance has listed to reinforce the theme that the UAE’s 9 per cent rate is the ‘lowest in the region’ and ‘one of the lowest in the world’.

Tax on assets

Apart from the tax-free status for corporate restructuring, there will also be ‘no tax on assets owned pre-corporate tax implementation’, the UAE Ministry’s note points out.

“Many companies operating in UAE would have immovable assets which are in use and been fully/partly depreciated,” said Atik Munshi, Managing Partner at Finexpertiza UAE. “Even though their fair value is higher than the book value.

“Here, the law allows such companies to fair value such immovable assets in the first period, so that they do not have to pay a high tax on disposal of such assets in the future.”

The Ministry’s updates come as corporate tax registrations gather pace after the tax authorities restated the deadlines by which businesses should be completing this key process.

Now, with its statement on the tax reliefs available, the Ministry is showing all the options that are available to businesses. (The first corporate tax payments under the new rules will start from September 2025, for companies that operate under the January to end December financial year.)

Heavy M&A activity

The UAE corporate scene has been witness to heavy merger and acquisition deals through the recent past. The corporate tax restructure relief will not apply in deals where there is only an equity stake sale.

One notable relief is the revaluation of assets in the first taxable year, in view of the first-time adoption of the UAE Corporate Tax regime

How does the restructuring relief work?

Any transaction that results in shares or ownership interests being exchanged between business entities will be eligible for relief. That way, ‘gains or loss are not taken into account in determining taxable income for either entity subject to fulfilment of certain conditions,” said Rakesh Nair, Director for Corporate Tax at the consultancy Crowe UAE.

Business owners should not that they should apply for relief if any such restructure process is going on. This must be made in their tax returns for relevant tax period.

Here are two typical examples when the restructuring relief would come into action:

- Situation 1: Person A has two businesses in agricultural goods trading and another in metals trading. Person A transfers the metal trading business to Person B in the form of shares or ownership interest.

- Situation 2: Company A merges with Company B and where Company A ceases to exist. Company B issues shares or ownership interest to the owner of Company A.

"Where corporate restructuring relief applies, the assets and liabilities transferred will be treated at their net book value," said Nair.

“Any unutilized tax losses incurred by the business making the transfer prior to the deal may be carried forward into the new arrangement, provided it continues the same or similar business.”

For UAE businesses lining up a possible M&A or a major restructure, this tax relief can be quite handy. Just make sure they tick these boxes...

- The transfer of shares is undertaken in accordance with the applicable regulations in the UAE.

- The taxable entity is resident or a non-resident with a permanent establishment in the UAE.

- The entities follow the same financial year and prepare financial statements using same accounting standards.

- The transaction is undertaken for valid commercial and economic reasons.